Oils

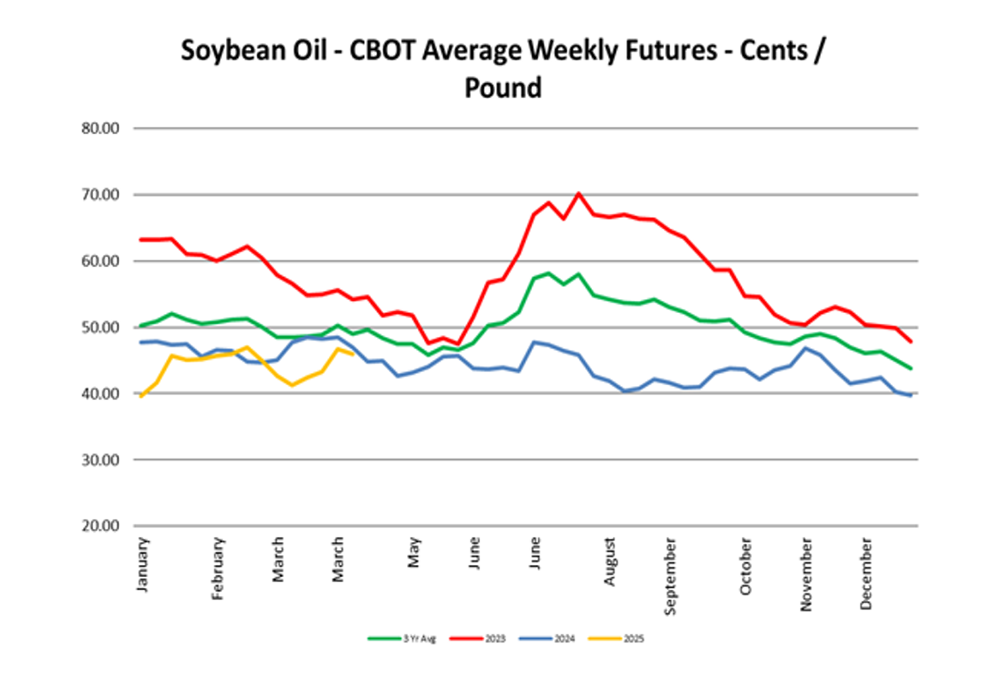

Sizeable increase for soybean oil and Canola this week. Palm is moving lower.

Beef

The number of cattle on feed, April 1 COF total of 11.638M head was 1.6% or 188,000 head lower than a year ago.

Download Our PDF for this report

Sizeable increase for soybean oil and Canola this week. Palm is moving lower.

The number of cattle on feed, April 1 COF total of 11.638M head was 1.6% or 188,000 head lower than a year ago.

We are seeing better availability across the industry. Breasts of all sizes are starting to steady out. Tenders demand has increased due to breast prices. Wings are readily available and the best value in chicken. Thigh and leg meat has been seeing heavy demand and tight supplies.

Ham markets are rebounding with improved interest from Mexico. Bellies remain unsettled. 42’s are unsettled as availability is not clear, while 72’s are steady. Loins are mostly steady. Butts are steady. Spareribs are steady while Louis and backs are not.

Offers are showing across the animal, as packers continue to address increasing inventories. Middle meats appear to have plateaued and packers are trying to entice buyers. End cuts continue to be adequate. Grind position remains steady, as the supply / demand remains balanced for the time being.

Shell egg markets are flat and California eggs are down. The Block & Barrel are up. Milk availability is growing in US as spring is peak milk production time. Butter is up. There is still more than enough cream available and there is export interest.

Mexican volume continues to decline as Peruvian picks up slowly. Some local volume has started which will help with supply. Markets continue to escalate as the holiday pull has further weakened supply. Demand exceeds supply continues throughout the week.

East – Supplies are good. quality is good, demand is good, and the market is steady

West – Limited volume on green as fields age, seeing mostly choice creating two tier market. Expected trend until California start up in three weeks.

Market holding mostly steady as supplies look good into next week and keeping up with demand. Quality is good.

The market high and continues be very active; total industry supplies are well below normal, and demand is strong Quality is reported as fair to good.

Market is down as supplies improve and keep up with the moderate to good demand. Quality is good.

Market is mostly steady with good supplies and moderate demand. Quality is reported as good.

Market is steady on Cilantro and parsley with moderate to good demand. Quality reported as good on both.

East – Supplies are tight, quality is good, demand is strong, and the market is increasing.

West – Beans remain very short with no relief for 10-12 days. Quality is fair. Market higher.

Market lower as Salinas is starting to getting into better volume and normal weights. Quality is reported as good.

Market is mainly steady as we settle in Salinas on moderate demand. Heart market is steady, and quality is fair to good for both.

Supplies are good. Washington will go thru May. Idaho has finished. California and Texas have good availability of new crop. Prices are steady in all areas with no quality concerns.

Supplies and quality remain good. Sizing is spread across all sizes making for consistent pricing from large to small. Quality is good. Prices are steady.

East – Supplies are good, quality is good, and demand is good, and the market is steady.

West – Plentiful supply with good to excellent quality reported. Market is lower.

Tomato markets are starting to increase on all varieties out east due to the transition into the Ruskin/Palmetto FL growing region. Out West, availability out of Mexico into the US was reduced due to the Easter holiday. Expect 1 week of elevated markets.

Mexico – Market prices continue to fall on 60’s, and larger. Small fruit remains in high demand and the market is getting stronger on 70s and 84s. Volatility will continue through May. California – Size curve is peaking on 48 & 60ct. Volume on Grade 2 is low.

Lemons – Supplies are steady, quality is excellent, demand is strong, and the market is increasing. Small fruit has tightened up as sizing has shifted to 115s and larger. Suppliers will be holding to 10–week averages through the next 4 to 6 weeks.

Oranges –Supplies are steady, quality is excellent, demand is strong, and the market is increasing. Small fruit is starting to tighten as smaller independent suppliers are finishing up. Suppliers will be holding to 10-week averages thru the end of the Navels.

Limes – Supplies are tight to start out the week, due to lack of harvesting last week in observance of Holy Week. The market has increased due to strong demand and tight supplies, anticipate this trend to continue until pipeline is replenished.

Supplies are tight, quality is good, demand is strong, and the market is steady. The industry is still dealing with vessel congestion at the Panama Canal and container inventory is still running low.