Beef

The Price declines during last month have been broad based, with all the major primals losing ground. Since March 21, the round primal has declined 6.6%, chucks down 5.5%, loins down 5.9% and ribs down 8.2%.

Download Our PDF for this report

The Price declines during last month have been broad based, with all the major primals losing ground. Since March 21, the round primal has declined 6.6%, chucks down 5.5%, loins down 5.9% and ribs down 8.2%.

Breasts evened out this week. Wings demand has strengthened. Tenders demand is strong and tenders remain the hardest offering to find. Dark meat demand remains very good. Whole birds are mostly balanced.

Butts continue to move up faster than predicted. Demand for butts continues to increase and will continue as we get closer to the holiday. Ribs are flat next week as demand as subdued the time being. Loins are also moving up due to retail interest and strong exports. Demand for bellies remains strong and the market continues to be volatile.

Ribs and tenders remain soft, as buyers use caution keeping purchasing windows tight. Strips and top butts, though under same pressure. End cuts, insides and chucks, continue coming under pressure from buyer bids. With increased harvest the support to thin meats seems to be slowing. Grinds continue mixed due to an irregular supply and expected improvement in demand.

Shell egg markets are all down and demand has softened. Cage-free supplies have surged by 22.2% over the past four weeks, despite significant production disruptions caused by the bird flu. The Block & Barrel are increasing and steady. Butter is down and Butter makers indicate both salted and unsalted production is taking place.

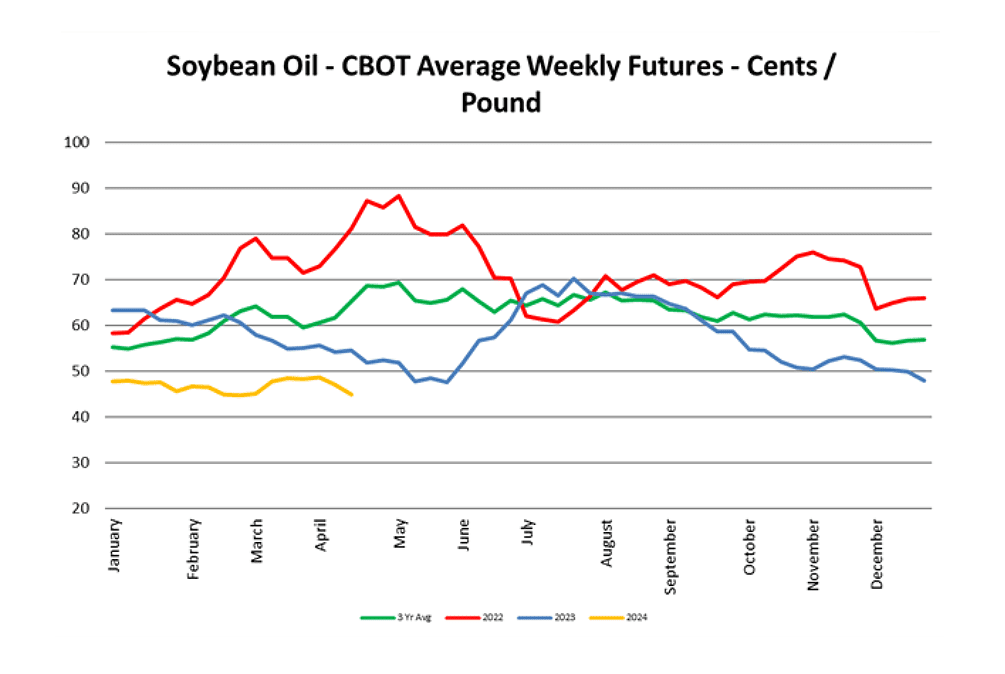

Soybean oil futures moved almost 5% lower last week with good harvest data coming from South America, good planting conditions in the US, and soybean oil stocks building. Canola futures in CA moved lower, keeping step with soybean oil, and exports are low. Palm is finally giving back ground due to soy prices.

While food service sales remained stable during the Lent season, escalating labor, energy, and other operational costs have led to an increase in prices. This poses a challenge to sustaining sales throughout the year. Post the Lent season, the anticipated surge in summer demand is expected to stimulate shrimp sales.

Peru volume has increased, Mexico is slightly lower, and local production underway. West market slightly higher but should steady out. East market slightly lower.

East – Green supply strong, quality is good, demand good and Market steady. Red and yellow bells easy to get, quality good, and markets lower.

West – Growing region shift taking place this week. Quality is excellent with dark green color and thick walls. Red peppers are lighter supplies with some reported quality issues, market slightly higher.

Weather and cooler night temps are still low and slowing production and keeping supplies on the lighter side, growers just keeping up with demand. Market steady.

Supplies and quality good on both red and green. Market mostly steady on both.

Market higher as cooler weather continues to limit growth, lowering yields, and demand is beginning to exceed supplies.

Cilantro market steady on decent supplies. Market steady on curly but flat is active as supplies are tight, expect demand to exceed supplies for the next couple of weeks.

East – Corn supply lighter, demand good, market stronger, and quality good.

West – Moderate supplies out of Imperial Valley, good demand, market steady.

Both Lettuce and Romaine are seeing an industry–wide quality issues that have push markets back up. Expecting tight supplies to the end of the month.

Availability continues to improve on jumbo and medium yellows, but larger sizes are limited. Rain in Texas has slowed down the harvest. Reds are limited in supply from all areas and will remain so for another few weeks. Whites are in good supply.

East – Chili pepper is a tight item – South Florida has finished up and Georgia has not started yet; limited availability resulting in higher markets.

West – Demand exceeds with no relief for 2–3 weeks, most affected are Serrano and Jalapeno.

Supplies are very light on 40–50 ct from most suppliers. 90–120 ct are plentiful. This now looks to be the case through the summer months. Demand is following supply accordingly. Prices are steady on large and lower on smaller sizes.

Rounds remain on alert status both east and west due to lack of availability. Roma markets are escalating due to a lack of availability both east and west. Grape & cherry markets are stable with normal demand.

East – Yellow squash and Zucchini has started in South Georgia. Most shippers are finished in Florida. Volume is very heavy on Zucchini and on the lighter side on Yellow Squash.

West – Moderate supply and demand. Market is slightly higher for zucchini, yellow lower others steady.

Pricing on large fruit continues to climb as growers are pushing for higher prices ahead of the Cinco holiday.

Lemons –Alert– There’s a significant shortage of small-sized lemons, with crops mainly in sizes 75’s, thru 115’s. San Joaquin Valley lemon crops are ending, and all supply mainly comes from Coastal California.

Oranges –Alert– Navel Oranges: Supply remains low, especially for small and medium sizes, as the season nears its end with (2-3 weeks left) for most shippers. The transition to Valencia oranges brings more large-sized fruits in San Joaquin Valley but Riverside will have medium and small sizes.

Limes – The stage of the new crop, 70–80 % of volume is in small sizes: 230’s/250’s.

Besides it being a new crop, during this time of the year we have very high temperatures and minimal to no rain in harvesting regions, which is slowing growth.

Slight relief in the market due to supply volumes that arrived as expected and planned. Situation remains fluid as strategic inventory based on quality of fruit and volume to hold through till mid May Mexican supplies arrive.

Volume will remain tight for another 2–3 weeks on large sizes. Climate was not allowing for fruit to mature as soon as expected. The market will remain tight for another 2–3 weeks. No logistics delays expected.