Beef

Placements in May were over 2 million head, 4.3% higher than a year ago. In the near term the inventory of market ready cattle has been coming down, which helps explain why feedlots appear to be in a better bargaining position.

Download Our PDF for this report

Placements in May were over 2 million head, 4.3% higher than a year ago. In the near term the inventory of market ready cattle has been coming down, which helps explain why feedlots appear to be in a better bargaining position.

Wings and tenders continue to be hottest part of the bird and excess supply is nonexistent. The wing market continues to show growth despite being off season. The jumbo breast market is seeing demand increase. Medium and small breasts have evened out. Dark meat demand remains very good. Whole birds are mostly even.

Butts are on the rise again and should see one or two more weeks of gains before the market falls off. St. Louis ribs and spareribs had slight gains while back ribs held flat going into next week. Boneless loins are declining as demand is still weak on these items. Bellies seems to still be on a trend of declining but the futures remain volatile.

Close in pricing is firm; although, post-holiday pricing reflects a more open to trade feel from packers. Middle meats continue to trade steady across the strip, rib, and sirloin sub-primals. Tenderloins continue to trade under pressure from lagging consumer demand. Insides, chucks, and grinds continue steady; due to need for lean material for holiday grind ads.

Shell egg markets are down this week. California and Northwest markets are flat. The Block & Barrel are decreasing. Butter is flat and production levels have weakened. 27 states remained under a heat advisory and heat puts stress on cow’s milk production as well as chickens egg production.

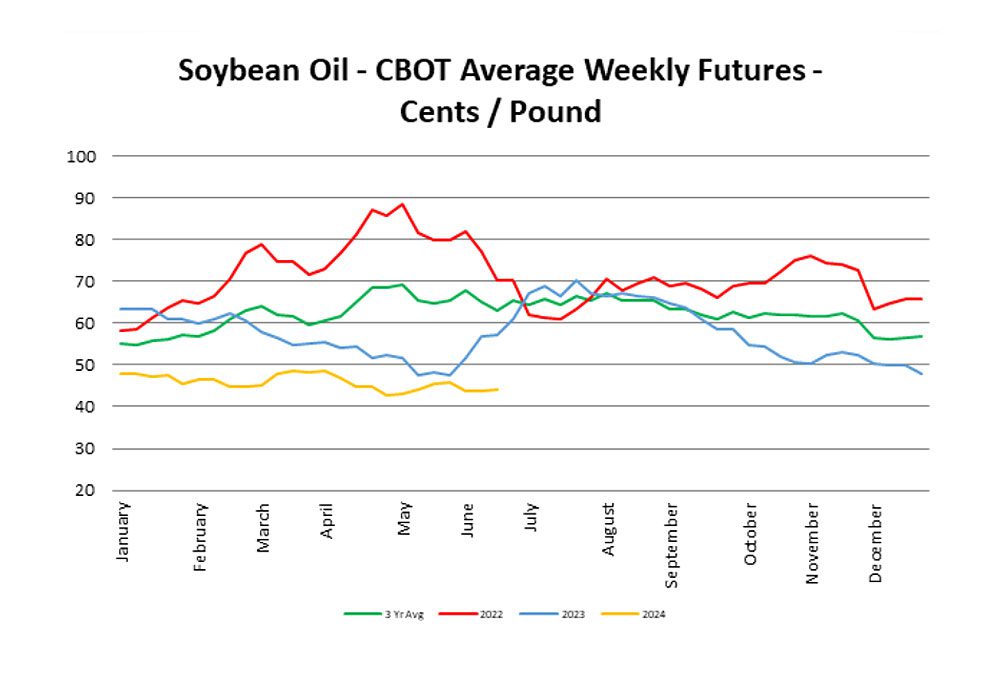

The soybean oil market continues trading flat. Next week we expect the USDA acreage report. There are some concerns for upper Midwest growing regions as they are very wet. Canada, too, has some very wet weather causing some concerns, which have not yet made its way into pricing yet. Palm supply and demand is balanced.

Market has reached a demand exceeds dynamic as both Mexico and Peru struggle to keep enough production coming to fill orders amidst a holiday demand pull. Mostly affected are Jumbos and Extra Large.

East – The green pepper market is strong. Georgia is finishing up and North Carolina is in full production. Markets remain high and are expected to stay higher for the next few weeks.

West – All varieties of peppers are limited in volume with red and yellow mostly affected. Regional growing shift, uncooperative weather have quality just fair at best. Market is very high and expected to hold up to ten days.

Market remains elevated and supplies remain tight. Supplies look to slowly improve and expect the market to see a slow downtrend over the next week or two.

Demand is exceeding supplies and market pricing continues to move higher. Seasonal quality and transitional challenges have significantly reduced yields at the field level.

Market lower as we settle into Salinas, and supplies continue to meet demand.

Good to moderate supplies with lighter demand keeping markets steady to lower.

Tight supply continues and Cilantro and market is firmer with demand exceeding supplies with many growers. Parsley markets active as Italian Parsley supplies remain limited, and quality is fair, curly parsley supplies are better.

Better supplies and yields continue to move up. Strong demand is keeping the market from dropping quickly but is trending down.

Romaine has started to settle and heart markets continue the slow downward trend, as supplies and quality improve.

Supplies are good on yellows and reds in New Mexico and California. There is rain in the forecast in New Mexico that could turn the market around. Demand is good. Quality is good. White demand and prices are increasing due to rain in Mexico and Central America.

Supplies are light on 40–50 ct from most suppliers. 90–120 ct are plentiful. This now looks to be the case through the summer months. Demand is following supply accordingly. Prices are steady on large and lower on smaller sizes. Quality is good.

East – Squash and zucchini markets are flat. Georgia is finished but most other northern regions have started.

West – Has volume increases on the coast and valley so seeing a much lower market. Yellow Squash volume is improving and market relaxing somewhat.

Supply continues to be light on all varieties (round, roma, grape, & cherry). Out east, the transition to AL has started, but volume is limited. Availability out of VA/NC will not start until early July. Out west, Norther California has started, but it may be another 1–2 weeks before we see any increased volume.

Mexican imports into the U.S. remain suspend except for one region. Rain is also limiting harvesting, although other regions are supplementing, we are expecting significant shortages until crossings are resolved. It is uncertain at this time as to when the border will re–open.

Lemons –Alert– Imports are arriving and will continue to increase from late June into early July. California is still experiencing a shortage of 165 to 200–count . General lemon demand remains strong. Demand is very active and exceeds supply. Market will be tight through the summer.

Oranges –Alert– Re–greening due to summer heat is upon us, but with no effects on taste, just appearance. Extra time may be needed to gas Valencia’s to bring on colour, which may cause some loading delays at packing houses.

Limes – Due to recent tropical storms, growers experienced reduced harvesting and packing operations, resulting in lower crossing volumes and increased prices. However, with the rain we anticipate volume improvements in the coming weeks which should start to stabilize pricing.

Supply remains tight, especially for larger sized fruit, and demand is very good. Big sizes are at a premium right now. Quality remains good.

Mexican volume is meeting demand with San Joaquin slated to start in a stronger way early July with no issues to supply. Market is steady.