Poultry

Hatch–ability remains an issue across the Chicken industry resulting in 3–4% decrease in hatch. Supply is tight across most offering but especially in wings and tenders which are the smallest part of the bird by weight.

Download Our PDF for this report

Hatch–ability remains an issue across the Chicken industry resulting in 3–4% decrease in hatch. Supply is tight across most offering but especially in wings and tenders which are the smallest part of the bird by weight.

As hatch–ability of eggs remains an issue across the industry and we continue to see supply shortages especially on wings and tenders. Breast demand is high on all sizes and excess supply is non–existent. Tenders and wings remain the hardest offering to find. Dark meat demand remains very good. Whole birds are mostly even.

B/I in butts are moving up next week while boneless butts took a slight dip. Spareribs are also moving up with grilling season approaching. Loins are also moving up as retail ads are being featured and strong exports. Bellies are moving up next week and the market remains volatile.

Packers continue talking of reducing harvest, buyers “pump the brakes” and look to clarify market direction. Ribs, strips, and tenders as the week progresses are leveling. Strips and top butts continue to be shinning stars of this market and are solid performers. End cuts, insides and chucks, are flat. Grind demand continues to improve.

Shell egg markets are all flat. The Block & Barrel are increasing and steady. Butter is up. The EU market still feels firm with milk production underwhelming and cheese absorbing more of the milk. Domestic butter demand is steady from retail and food service sectors. However, for unsalted butter loads, demand is stronger.

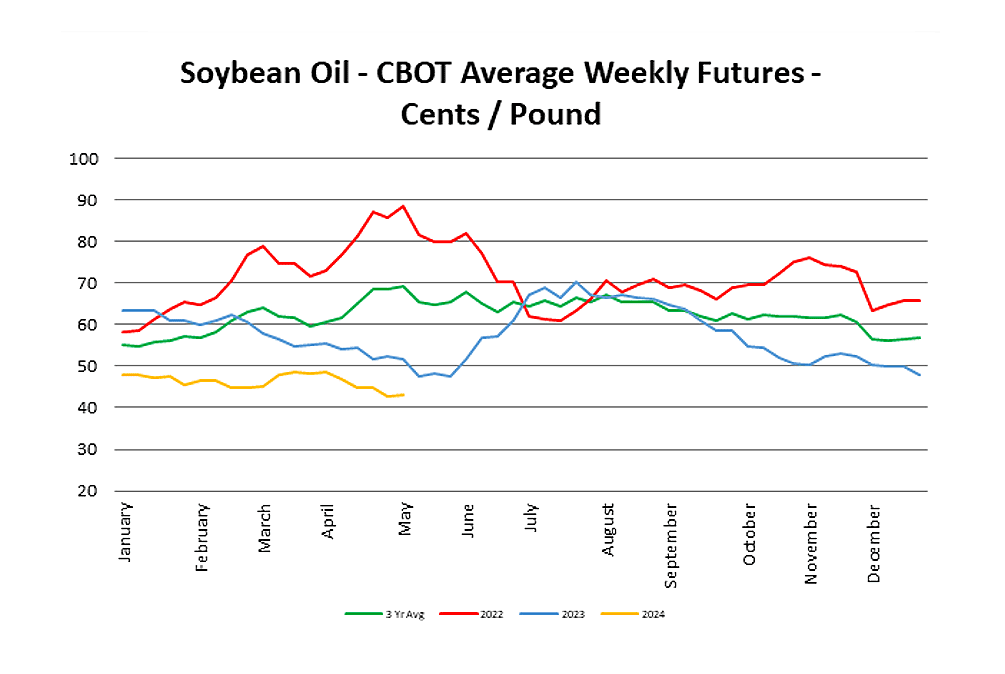

Soybean oil futures were volatile last week but ended just over 1% higher. Pressure from palm oil helped move the market higher, and possible tariffs for used cooking oil, possibly adding more demand to soybean oil. Canola oil moved along with soy. Palm was higher, but not sure why. Supply is higher and demand has declined.

Import volume coupled with local are expected to keep this market steady. With the delayed Peruvian vessel hitch causing a slight spike the eastern market should settle down some. Larger sizing should remain tight.

East – Green bell supply lighter, demand good, new growing areas with weather impacting supply. Market increasing. Red and yellow bells are limited, demand good, and market increasing.

West – Steady supply, market with moderate demand. No expected changes.

Market increased due to lighter yields and higher demand. Some local regions are light increasing west coast demand. Supplies are adequate to meet demand.

Market continues trend higher on red and mainly steady on green on the west coast.

Market continues to come down as supplies continue to improve and demand is moderate.

Supplies remain snug and market remains firm. We do not anticipate any significant relief until Salinas starts up in June.

Cilantro market firmed up on lighter supplies. Market steady on curly Parsley but flat is active as supplies are tight, expect demand to exceed supplies for the next couple of weeks.

East – Corn will have good supplies out of Florida. Georgia should start up in a small way in the coming weeks. Quality has been very good.

West – Demand is fairly light but expected to improve. Market is slightly lower.

Quality improving with better weather helping. Supplies remaining light keeping markets firm on the stronger side. Demand remains strong and suppliers are just meeting current demand.

Yellow onion supplies are increasing due to New Mexico starting up. California remains steady and Texas is declining. Reds are still in limited supply from all areas and will remain so for the next couple weeks. Yellow and White prices are declining. Reds are steady.

East – Hot pepper supply better, quality good, demand weaker, and markets lower.

West – Limited supplies with new growing regions just starting. Demand remains moderate market is high but steady.

East – Zucchini and yellow squash supply is steady quality good and markets a bit lower.

West – Transition week for squash as Mexico finishes and California starts, no expected gap with light demand, market is steady.

Round markets continue to improve with increased availability out of Florida. Grape and cherry markets remain stable with steady volume on normal demand. Roma markets are increasing due to declining volume out of MX.

Pricing has stabilized and expect current levels to hold for the next couple of weeks. 48’s and larger will remain at a premium compared to 60’s and 70’s.

As Offshore volume declines and demand increases, we have a spike in the market. Expected volatility 7–10 days. Sizing flexibility may be necessary to fill orders.

Lemons – Alert – District 1 fruit is mostly Large (115 & lgr). Consequently 140s & smaller are very tightly supplied. D2 Lemons have a larger size structure as well due to the rain in SO California this winter. The lemon market will continue to be tight throughout the summer until imports start to arrive.

Oranges – Alert – Navels peaking on 40/36/56ct size. Exports have finished. Small size oranges are very tight due to navel size structure. Smaller sizes are better supplied, yet still tight due to less packinghouses running Val’s.

Limes – We continue to see increased overall availability as weather trends become more favorable for accelerated growth. The crop is currently peaking on 230’s & 200’s; yields on 175’s are also increasing in volume. Large sizes 110s/150s are still limited in supply.

Steady supplies with final Peruvian expected to land in 10 days. Mexico start up underway with Green seedless, reds to start within the next week. Tiered market as importers work to clear inventory. Focus will be on quality.

Production volume has improved on 6ct and 7ct. Size 5 is still very tight. This is expected to continue for another 3 weeks. No significant peak is expected this summer.