Beef

March’s total supply of beef in cold storage was 9.5% lower than a year ago. This could reflect industry challenges. Key factors: drop in export business, limited facility capacity, high interest rates or lower production.

Download Our PDF for this report

March’s total supply of beef in cold storage was 9.5% lower than a year ago. This could reflect industry challenges. Key factors: drop in export business, limited facility capacity, high interest rates or lower production.

Random breasts are seeing increased demand due to Cinco de Mayo. Wings demand has strengthened. Tenders demand is strong and tenders remain the hardest offering to find. Dark meat demand remains very good. Whole birds are mostly balanced.

B/I butts demand was soft last week driving the market down just slightly. Boneless butts are moving up as demand is still strong. Ribs continue to gain strength as grilling season is approaching. Loins are being featured in retail ads driving the market up. Bellies again are volatile but are coming down next week.

Supply is outpacing demand across the complex. Short loins, top butts, tenderloins, and brisket due to seasonal demand are in the best position. Ribs, strips, and thin meats continue losing ground. End cuts, insides, and chucks are coming under pressure from buyer bids. Grind demand has improved and with holidays and grilling weather ahead.

Shell egg markets are all down and demand has softened. The Block & Barrel are increasing and steady. The number of loads showing up on the spot market has slowed from 71 three weeks ago to just 9 so far this week. Butter makers are running busy production schedules and continue to build bulk butter inventory.

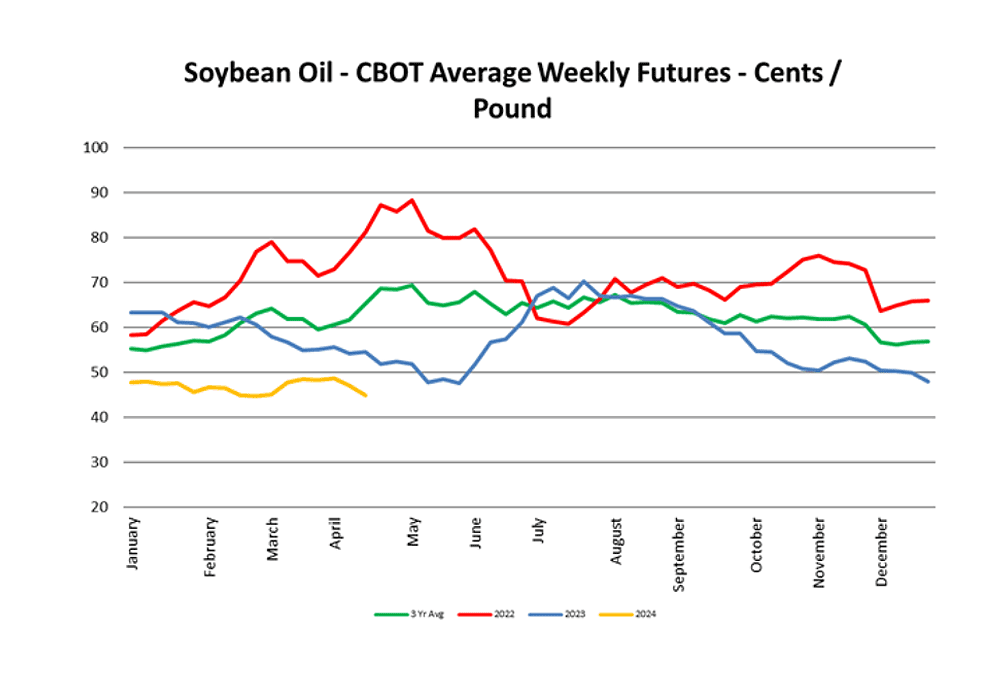

Soybean oil was slightly higher last week. South American harvest is just about done but there are rumors of Argentinian strikes are causing export delays. Wet weather in the US has slowed planting but it’s not a concern. Soybean oil is bearish. Palm is tight with production concerns. Canola is moving with soybean oil.

Mexican volume is limited as growing regions transition, Peru volume has increased as well as local. Markets are slightly higher and quality is reported good.

East – Green bell supply better, quality and demand good, and market lower due availability all over Florida. Red and Yellow at their lowest level in years, quality and demand good.

West – Green supplies are good out of the desert are peaking but should lighten up. Reds and yellow supply to improve mid–May, for now reds are good, expecting lighter supplies and higher pricing on yellows. Quality is good on all.

Market mostly steady to a bit lower as volume is fairly steady and meeting demand.

Market jumped higher on red and up a bit on green on the west coast.

Market higher as cooler weather continues to limit growth with supplies expected to be tight the next two weeks. Demand exceeds supplies with a number of growers.

Some shippers are light on volume, while others are in good supply, keeping this market active.

Cilantro market steady on decent supplies. Market steady on curly but flat is active as supplies are tight, expect demand to exceed supplies for the next couple of weeks.

East – Supply and Quality out of Florida is excellent. Good supply around keeping markets very soft.

West – Moderate supplies with no expected changes.

Supplies are very light on 40–50 ct from most suppliers. 90–120 ct are plentiful. This now looks to be the case through the summer months. Demand is following supply accordingly. Prices are steady on large and lower on smaller sizes.

The volume remains very light for both romaine and hearts. The weather has been inconsistent, and quality issues persist impacting yields. Markets and demand remain very strong. Expect supplies to be tight for 2–3 weeks.

Yellow supplies in Texas are decreasing. California volume is increasing. Reds are limited in supply from all areas and will remain so for the foreseeable future. Whites are in good supply. Yellows are steady from last week. Reds are higher. Whites are steady.

East – Hot pepper supply very limited, quality good, demand very strong and markets very high.

West – Demand exceeds due to light supplies and increased demand. Market high and holding. Relief expected in two weeks.

Supplies are very light on 40–50 ct from most suppliers. 90–120 ct are plentiful. This now looks to be the case through the summer months. Demand is following supply accordingly. Prices are steady on large and lower on smaller sizes

Zucchini and Yellow squash supply plentiful, quality good, demand good at lower prices.

West – Good supplies and quality out of all growing areas. California is slated to start next week. Market is low.

Rounds remain on alert status, but larger round fruit availability is improving out of Ruskin & Palmetto FL. Grape & cherry markets continue to improve with increased availability on normal demand. Roma markets remain stable.

US market pricing will remain relatively flat. There is more availability of small sizes than large sizes, and we expect this trend to continue. Quality remains fair.

Lemons –Alert–There’s a significant shortage of small-sized lemons, with crops mainly in sizes 75’s, thru 115’s. San Joaquin Valley lemon crops are ending soon, then supply mainly will be Coastal California that will help smaller fruit.

Oranges –Alert–Navel Oranges: Supply remains low, especially for small and medium sizes, as the season nears its end with (1–2 weeks left) for most shippers. The transition to Valencia oranges brings more large–sized fruits in San Joaquin Valley but Riverside will have medium and small sizes.

Limes –The industry will continue to see increased availability on small sizes; large sizes will become more limited in supply. Due to an extended period of lack of rain, scarcity of large fruit will likely continue throughout the month of May.

Greens Mexican harvest has started in a slow way which is helping the market find a slight balance. Tiered quality market as aggressive pricing for lower quality surfaces. May focus will be volume execution of quality product.

Demand remains strong and exceeds supply across all categories. Pineapples are still tight overall, but export volumes are strengthening. Next week should see slightly increased volumes which are expected to increase week over week.