Beef

Cattle slaughter came in at 586k. This was the lightest, non-holiday week, slaughter we have seen since end of March. Packers have been dropping the weekly harvest in the past couple weeks as their margins drop.

Download Our PDF for this report

Cattle slaughter came in at 586k. This was the lightest, non-holiday week, slaughter we have seen since end of March. Packers have been dropping the weekly harvest in the past couple weeks as their margins drop.

Bigger birds, better hatchability, and larger egg sets are allowing extra supply on the market, especially in the boneless market. Tenders and breasts are seeing increased supply on all sizes. Wings are seeing extra availability on larger sizes. Small wing availability is tightening. Dark meat demand remains very good.

Butts both Bone–in and boneless are trading near established price levels. Loins are steady–again, demand continues to be down. Ribs are mixed–spareribs are ramping up for new year’s, while backs and louis are steady. Bellies are steady and the market is increasing slowly since mid–September. Trim is steady with minimal increases on the week.

Packers once again had to pay higher for cattle and were also able to lower the weekly slaughter which helped push prices higher across most all cuts. Ribs, tenders, strips, and short loins saw the largest increases on the carcass. Chuck rolls remain very limited and are trading at four year highs. Rounds and thins saw modest increases. Market is expected to continue to stay strong.

Shell egg markets are up this week. California and Northwest markets are up. Two farms were identified as HPAI positive over the weekend in Washington & Utah. The Block & Barrel are decreasing. Spot Cheese markets are falling faster than expected. Butter is down.

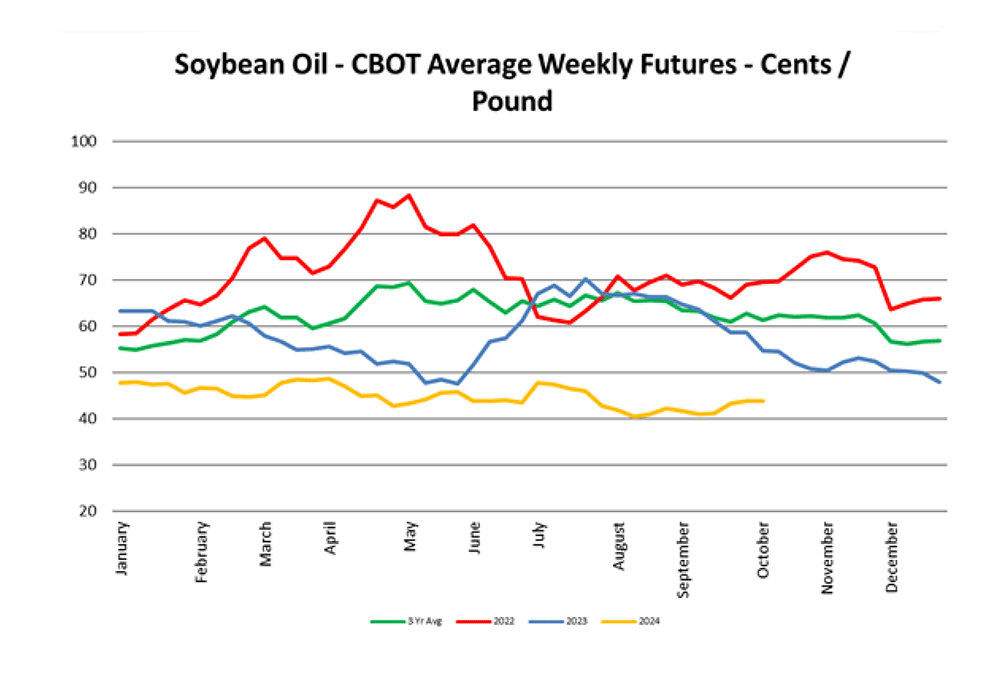

Soybean oil futures moved lower last week with excellent crop progress 10% above last year. Last week the WASDE report from the USDA was not very impactful to the market. Canola seed futures rose, Canola oil moved slightly higher. Palm continues to be higher. Corn, soybeans, meal, oil, and wheat all moved lower.

Volume has improved and is meeting demand this week. No expected changes for 2-3 weeks. Market is lower. Quality is good to fair.

Market is firm but as come down a bit, recent heat issues continue to impact yields and quality. Growers are keeping up with demand despite the lower yields.

Supplies are extremely limited from all suppliers due to weather-related quality issues. Currently demand is exceeding supplies.

West Quality continues to be poor, with very limited supplies, market is higher. Southeast corn continues to be in tight supply. Grower lost corn fields due to Hurricane Helene a couple of weeks ago. Markets are strong and supply.

Market is down, but still some quality issues impacting yields that could move this market up if demand picks up as supplies are just moderate.

Market mostly steady to a bit higher on moderate supplies. Quality has been reported as good.

Market steady on cilantro and high heat is impacting yields and keep market up. Parsley market mainly steady on fair to good supplies and moderate demand.

Demand is moderate to good, and supplies are a bit tighter on lower yields, market is up a bit. Extended heat expected to bring on some tip burn.

Market is steady on both romaine and romaine hearts. Both items are not abundant however most growers are meeting the demand currently.

Supplies are tight as new compost has reduced yields with some growers. Market is a bit active.

Supplies are good on new crop yellows and reds from Washington and Idaho. Demand is good. Quality has been good. Prices have stabilized on all colors.

Supplies are good on the new crop. The size so far is large with some growers being limited on small sizes. Quality is also good. Prices are slightly lower.

West – Stable volume and quality. California production is slowing down with Mexico crossing filling demand. Should be a steady transition.

East – Zucchini and yellow squash supplies lighter, demand better, quality is good and market increasing.

Tomatoes are on alert status due to low availability both east and west. Market is active on all varieties due to lack of product both east and west. Quality will vary greatly amongst shippers.

Harvest volumes have been strong, but fruit is slow to size up. 60s and smaller are readily available. 48s remain tight. 40s and larger are limited. Fruit is expected to continue sizing up and larger sizes should be more readily available mid-November. #2s remain in limited supply.

Lemons – Demand for lemons is steady. District 2 winding down. District 3 has begun for most suppliers. Chilean imports still have a few weeks to go and peaking on 200s /165s. District 3 is peaking on 165s, 200s, and 140s followed by 115s.

Oranges – Strong demand for oranges continues and supplies remain extremely limited. The industry is waiting for the New Crop Navel to be ready for harvest. Estimates are showing possibly picking Week of 10/14 or 10/21 depending on Color / Internals.

Limes – The lime market continues to decline. Crop peaking in 250/230s which is 60% of yields; coloring has much improved, however, due to high humidity/rain, increased skin breakdown/oil spots. Large sizes will be limited.

Supplies remain good and quality good as well. Not much change expected for the next 2 weeks, market is steady.